Food delivery giant Swiggy’s ambition to become the one-stop platform for urban convenience is undeniable, but when it comes to the business, profitability has remained inconveniently elusive.

Despite the major UI-UX overhaul last month giving the Swiggy app a new look, its Q1 FY26 financial numbers revealed a familiar picture: burn to grow.

At a time when the majority of the new age tech companies have turned profitable or are showing signs of profitability, Swiggy’s loss continues to grow both sequentially and annually. The company reported a net loss that zoomed 96% to INR 1,197 Cr in the June quarter from INR 611 Cr in the year-ago quarter. On a sequential basis, the company’s loss grew 11% from INR 1,081 Cr.

This was reflected in the company’s stock plunging by 4% the next day after the results.

The company has reached a point where all hope to scale now rests on Instamart. Ironic as it may sound, currently, it is Instamart that is dragging Swiggy to further red.

While Swiggy CEO Sriharsha Majety underlined that Instamart has grown out of the shadow of the food delivery business, the important question remains: when will the quick commerce arm start driving its growth?

Moreover, with Instamart’s plan to slow down expansion, the question that further sticks out is how Swiggy intends to scale and deliver profitability at the same time.

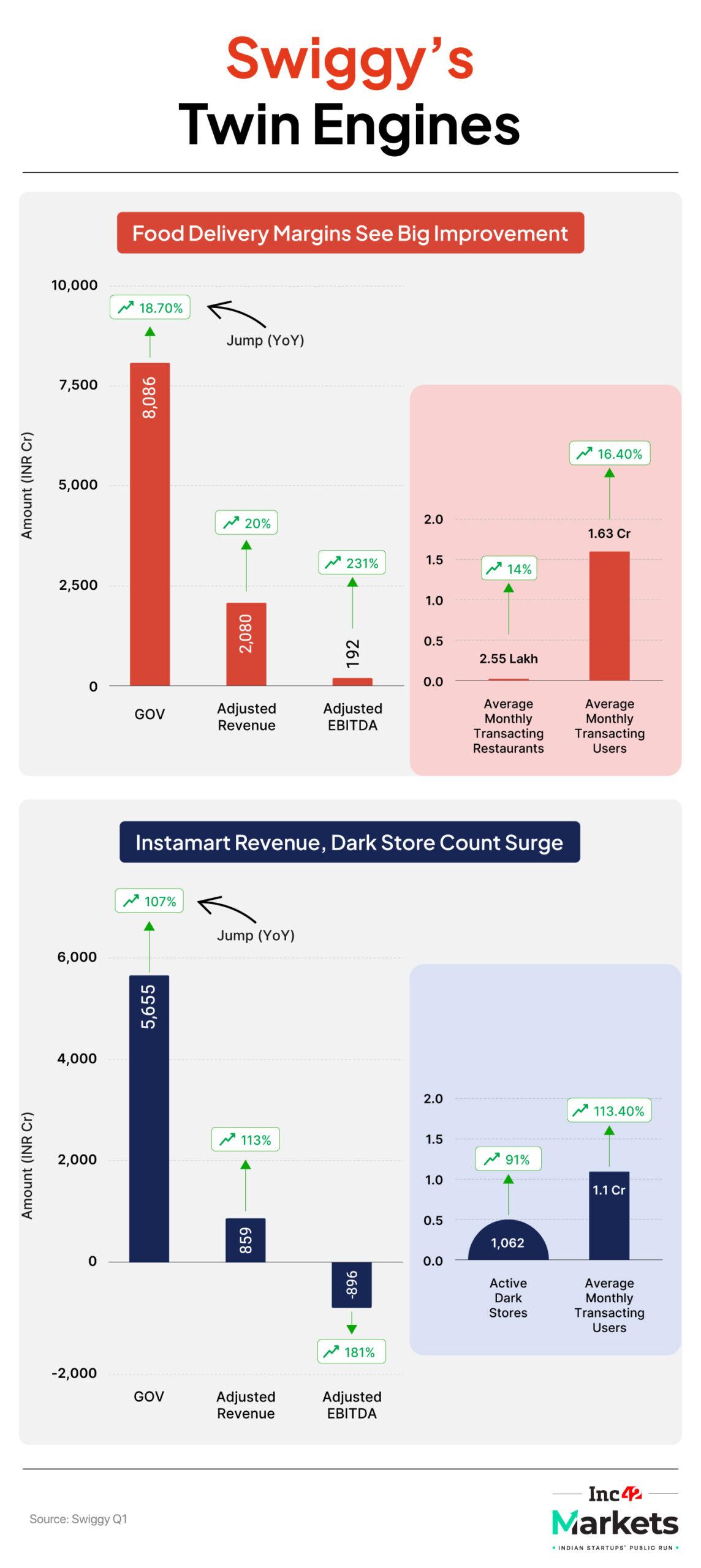

The quick commerce grew over 100% gross order value (GOV) in the Q1 FY26, contributing almost 40% of Swiggy’s overall GOV.

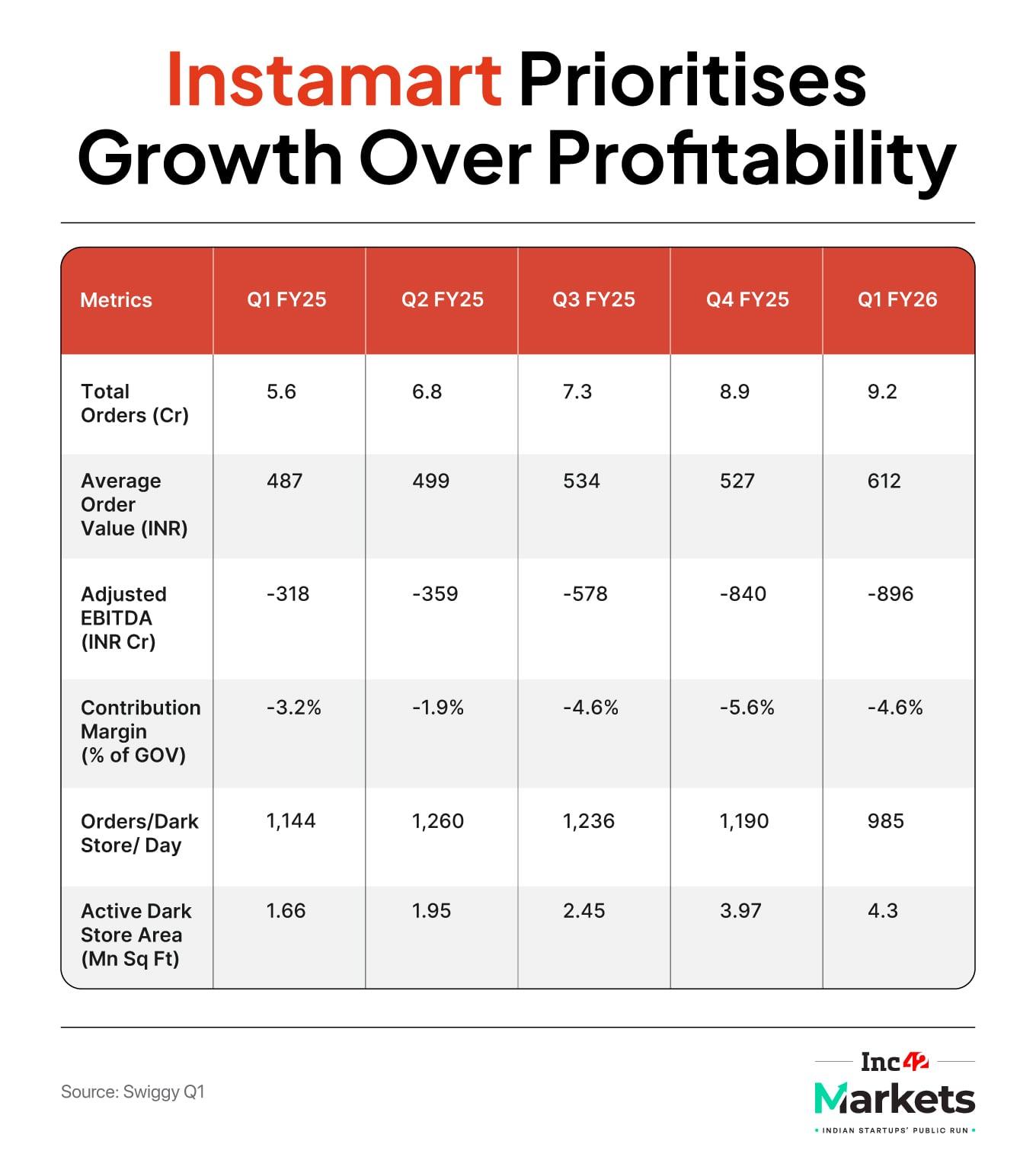

This growth has been fueled by the aggressive expansion of its dark store network. After adding 314 dark stores in Q4 FY25, Instamart added 41 in the last quarter. As a result, the quick commerce arms’ adjusted revenue surged by 113% YoY to INR 859 Cr during the quarter.

More importantly, the focus on expanding product assortment led to a total order count of 17.6 Cr, spurred by the gradual increase of non-grocery categories, which offer better margin value than the typically razor-thin grocery segment.

Instamart certainly seems to have grown out of the shadow of the food business in terms of GOV, but a closer look at the overall company’s financials reveals that Instamart continues to run on food business revenue. Instamart’s rising EBITDA losses of INR 896 Cr, against the food business’s profit of INR 192 Cr, is also a stark contrast that is hard to miss.

Of the company wide INR 319 Cr in capital expenditure incurred this quarter, about three-fourths was incurred towards warehousing capacity expansion and funding of the previous quarter’s darkstore expansion, and the remainder towards darkstore additions.

Swiggy’s cash burn against its cash balance is something that has compelled HDFC Securities to downgrade it to “Add” from “Buy” in the previous quarter.

Despite Swiggy Instamart’s growing loss, Swiggy’s top management reiterated its plan to achieve the contribution margin breakeven for Instamart between December 2025 and June 2026.

Will Instamart Shift Deliver Profit For Swiggy?Swiggy Instamart’s path to achieve breakeven hinges strongly on improving its average order value (AOV) significantly. In Q1FY26, Swiggy’s AOV jumped by 25.6% YoY to INR 612, signalling an early transaction to shift consumer behaviour from a low-order ticket to a larger basket.

A key catalyst behind this jump was the introduction of MaxxSaver, Swiggy’s equivalent of Zepto’s SuperSaver. This programme encourages users to increase their basket size by offering bundled savings and rewards for larger purchases, primarily monthly stock-ups.

You see, the concept of quick commerce was built on the idea of last-minute delivery or impulse purchase, but Swiggy Instamart, gradually moving away from this.

While an increase in basket value will call for a better discount, making a minor dent in the contribution margin on the short term, fewer deliveries will improve the overall margin. Besides, this is expected to create more customer stickiness.

“Our goal is to keep the AOV increasing with the help of MaxxSaver. Moreover, this programme has also helped us see an increase in repeat purchases,” Instamart CEO Amitesh Jha added in the earnings call.

In tandem with increasing AOV, Swiggy is also rethinking its infrastructure strategy. After a period of aggressive expansion of setting up dark stores, Swiggy seems to be applying the brakes on its expansion plans as it intends to leverage its already existing infrastructure network.

Instead of setting up small dark stores, Swiggy will be focusing on setting up larger stores – megapods with broader assortments and a higher throughput potential. This move will allow Instamart to stock up more non-grocery SKUs, to increase both AOV and margin.

The combination of increasing AOV along with low capital expenditure and growing non-grocery SKUs in the coming quarter has put Swiggy in a better position to improve its overall margins.

Moreover, dark stores that were set up in the last quarter of FY25 and Q1 FY26 are likely to show results in the coming quarters.

“With a pause on dark store expansion in ST and easing in competition (JEF view), 1Q profitability marked the trough. Swiggy, however, remains prone to high volatility due to a low margin base; U/G to BUY (high risk-reward),” Jefferies added in its note.

Food Biz Sees A New ThreatSwiggy’s food business continues to remain the company’s strong pillar. The food delivery business saw a steady growth of 18.8% YoY to INR 8,066 Cr, and the monthly transacting users reached a record high of 16.3 Mn. The adjusted revenue surpassed the INR 2,000 Cr mark, aided by newer formats such as Swiggy Bolt, Snacc, along with an affordability-focused initiative such as 99-store.

The strong performance of the food delivery business keeps the brokerage firm optimistic. While Morgan Stanley underlined that the growth in the food delivery business is living up to expectations, Jefferies highlighted that the food delivery business posted a “strong growth” in the quarter under review.

With that said, Swiggy’s food business, just like its competitor, Eternal, witnessed profitability challenges due to seasonal pressures. The food business’s contribution margin dipped to 7.3% and EBTIDA margin declined to 2.4% due to higher delivery costs stemming from the reverse migration of delivery executives, compounded by the annual employee appraisal.

While Bolt’s contribution continues to hover around 12% in the overall food delivery, concern persists around the drag from aggressive discounting products such as 99-Store, CrazyDeals, and PocketHero.

The competitive landscape is intensifying in this space with newer players such as Swish, Zing, and the anticipated entry of ride-hailing giant Rapido into the food delivery business poses a significant threat to both Zomato and Swiggy.

While Swiggy is likely to divest its INR 900 Cr investment in Rapido in the coming quarter, the larger concern remains with Rapido becoming a direct competitor, which is likely to dilute food delivery contributions, constraining capital allocation towards Instamart.

This is likely to bring down the contribution of the food business, leaving little capital for Instamart to grow.

The key concern for Sriharsha Majety and his leadership team is to steer Instamart to profitability within the given timeline. According to Macquaire, which maintains Swiggy with an “Underperform” rating on Swiggy stressed that Instamart will continue to risk Swiggy’s contribution margin breakeven timeline.

With BlinkIt widening its lead and inching closer to breakeven, the pressure is on Swiggy Instamart to deliver meaningful returns to retail investors before investor fatigue sets in.

- PB Fintech’s Q1 Snapshot: The fintech major’s consolidated net profit zoomed 41% to INR 84.7 Cr in Q1 FY26 from INR 60 Cr in the year-ago quarter. However, it slipped 50% from INR 170.7 Cr in the preceding March quarter. Operating revenue rose 34% YoY to INR 1,348 Cr.

- IndiQube Muted Public Listing: Shares of the workspace solutions provider listed at INR 218.7 apiece on the BSE, down 7.7% from the issue price of INR 237. The company ended the trading session at INR 217.9 on the BSE, down a marginal 0.37% compared to its listing price.

- JFS To Raise INR 15,825 Cr: The fintech major is looking to raise the capital via a private placement of convertible warrants to members of its promoter group. This comes at a time when the RIL-backed financial services major is putting its fintech super app plans into motion.

- Fino’s Q1 Profit Tanks: The payments bank’s net profit fell 27.4% to INR 17.7 Cr in Q1 FY26 from INR 24.3 Cr in the same period last year. Meanwhile, income from interest rose 34.4% YoY to INR 60.9 Cr. The reason for the decline in profit was a rise in tax expense.

- Jio’s $6 Bn IPO: Adding on to what seems to be a perennial discussion about Reliance Jio Infocomm’s IPO, Reliance Industries has initiated discussions with SEBI to sell a 5% stake in the telecom giant via an INR 52,465 Cr public listing.

- LEAP India Gears Up For IPO: The supply chain solutions provider has roped in UBS, Avendus Capital, IIFL and JM Financial as lead managers for its upcoming IPO. The company plans to file its DRHP with SEBI within the next few days.

- Go Digit’s Profitable Q1 Show: The insurtech company reported a net profit of INR 138.3 Cr in Q1 FY26, up 37% from INR 101.3 Cr in the year-ago quarter. The company’s gross written premium stood at INR 2,982 Cr in the quarter under review, up 12% YoY.

The post Has Swiggy Instamart Come Out Of The Food Delivery Shadow? appeared first on Inc42 Media.

You may also like

Ancient capital an hour from London has mystery tomb older than Stone Henge

Salt and vinegar need one other common item to kill gravel weeds for good

Inside world's biggest airport under construction with 12 square km of shops

Russiagate: Tulsi Gabbard says Russia believed Hillary Clinton's 2016 victory 'inevitable'; claims Obama admin orchestrated hoax

Universe Simplified Foundation brings hands-on science and tech education to under-resourced schools (VIDEO)